by Research Division HIMA ESP FEB UNPAD

Previous to the Covid-19 pandemic, the world predicted that the source of global recession and pressure from the political economy was indeed full of challenges, starting from the global financial crisis, debt crisis, geopolitical issues, US Normalization, trade war, domestic tension and so on. However, it turns out that the crisis that occurred in 2020 was caused by a pandemic, where this crisis did not only have an impact on the economic sector. Covid-19 became an authentic crisis which resulted in a demand shock and supply shock, and gave a domino effect to various sectors ranging from health, social and financial. The occurrence of the Covid-19 pandemic requires us to always be ready to face unpredictable sources of pressure in the future, so that sustainable economic development becomes even more crucial. The emergence of the Covid-19 pandemic at the end of 2019 in China then spread and is still escalating rapidly throughout the world and creating new waves in various countries ranging from countries in Europe and America, this has had a big impact starting from infected cases of 60.09 million. The death rate continues to increase, but the patient’s cure rate is also high which causes high uncertainty.

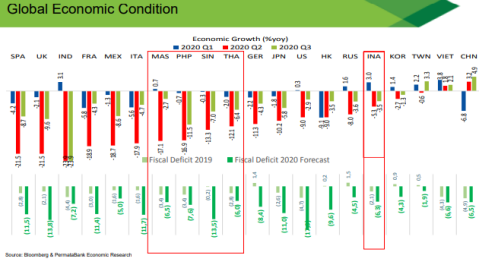

Handling Covid-19 is the initial key to economic recovery, handling Covid-19 based on the covid resilience ranking has implications for economic growth. Countries with covid resilience rankings fairly good such as China, South Korea, Vietnam and Taiwan have far better resilience to economic conditions compared to other countries.

The recession phase experienced by various countries began in the first quarter, while Indonesia experienced a recession phase since the second quarter. Based on the data above, it can be seen that the economic recovery has started to occur. Countries that rely on international trade, such as Malaysia, Philippines, Singapore, and Thailand, have contracted up to double digits, for this reason, in this condition, domestic consumption is the thing that most supports the economy. This can be seen from the widening of the budget deficit, which increased quite significantly due to the response of the fiscal policies of various countries in the world. When the economy is facing a crisis from the Covid-19 pandemic, people have a tendency to delay spending and saving. On the other hand, the fiscal deficits from various countries also widen, so the public sector has a role to play in filling domestic demand gap.

The Covid-19 pandemic case creates a direction of increasing cases that vary in each country, but there are certain patterns in each continent, this makes us unable to conclude what policies are right to do. For example, policy lockdown in which not all countries succeed with this policy, this is because each country has different human characteristics and demographics, so it cannot be handled in the same way. The escalation of daily Covid-19 cases in Indonesia continues and again creates new records with daily cases above 5000. The increase in cases still has to be watched out for so that in handling Covid-19 and economic recovery must work together in an effort to normalize, discipline and good cooperation are needed. from individuals and groups of society. In addition to the direction of the increase in cases and the pattern of the Covid-19 pandemic that varies from country to country, each province in Indonesia also has a different direction of increase in cases and the pattern of the Covid-19 pandemic, this is due to the ability of each province to do so. Testing and the availability of facilities that are owned, so that a comprehensive handling of Covid-19 is required down to the micro level.

In February 2020, China has started to implement strict restrictions in various areas, especially Wuhan, one of which is a lockdown. In the map below, it can be seen that the handling of the pandemic carried out by countries in the world is in stark contrast because they still do not consider Covid-19 as a threat.

The end of March is the peak of strict Covid-19 handling restrictions because Covid-19 has been declared a pandemic. Then from June to September it started to fade, but in November several countries returned to carrying out strict handling, this shows the characteristics uncertainty of the Covid-19 pandemic which gave high uncertainty, so policy options from various countries were needed to handle it. Loosening or tightening its policies.

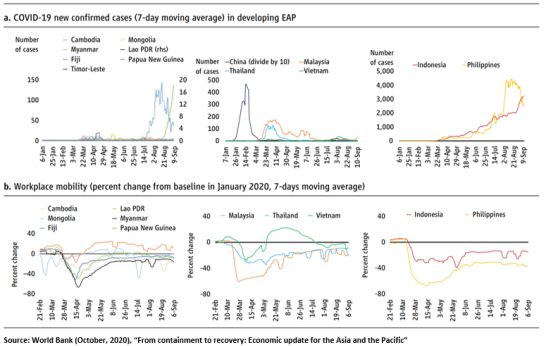

Based on the data above, the Covid-19 case is directly proportional to mobility, where if there are high Covid-19 cases, there will be high mobility or vice versa. This is important, because population mobility is a reflection of economic activity and is part of a leading indicator.

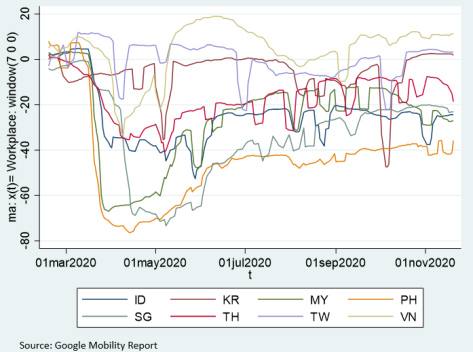

Based on a report from the Asian Development Bank, the data shows that the change in average mobility from baseline when moving from left to right signifies a decrease in mobility, while GDP growth decline is defined as GDP growth quarter reduced GDP growth in the future normal. This is an ideal indicator in understanding the problem not just economic growth year-on-year. This is because the impact of Covid-19 on economic growth must consider economic growth under normal conditions and not compare it with developed countries, because the growth of developing countries is usually greater than the growth of developed countries or can be called not apple to apple. The greater the reduction in mobility as a result of the policies implemented, the smaller than normal economic growth will be, so that mobility becomes a leading indicator in determining economic growth.

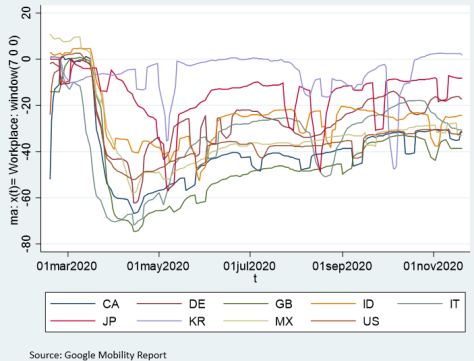

Based on the data above, it can be seen that Indonesia’s mobility is still decreasing, GDP growth and mobility have a negative correlation, this indicates that in Q4 there will be a risk that economic growth does not necessarily have good potential or is in accordance with what expected. Countries with better growth contraction than Indonesia, such as South Korea, Japan and Germany, have better mobility, while Indonesia is still struggling with mobility cases. This means that hopes for a quick and easy recovery are not shown by the latest data, therefore caution and anticipation is needed because the hilal has not been seen.

The financial sector is the sector that was first affected by the Covid-19 pandemic. Anxiety from investors at the height of the Covid-19 pandemic crisis is measured by the Volatility Index. It can be seen in March which touched a high number from the previous year, when Covid-19 made headlines and spread rapidly the financial sector began to absorb fear seen from its indicators. Because the uncertain handling of this has resulted in share prices, asset prices have dropped as investors started to play it safe. Not only does it have an impact on the financial sector, it also causes the perfect storm or a crisis that continues to spread in various aspects.

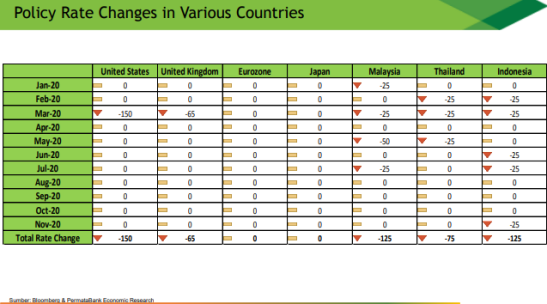

Central banks in various countries carry out super accommodative policies, meaning that the interest rates from the central bank tend to fall. The Covid-19 pandemic has pulled down the economic growth of various countries in the world. The lowest levels of economic growth occurred around April and May. However, the economic recovery has tended to be visible since August. This led to expectations that a recovery will continue to be seen in the next few quarters. If the vaccine has not been distributed or the success has not been seen, conditions in 2021 will still not fully recover from both the demand and supply sides. Vaccines are an important factor in 2021 for optimal economic recovery.

Based on the projection above, economic growth will tend to improve, although not significantly increase. In Q2-2021 there will be a technical recovery, because of the assumption of successful vaccines, increased public immunity, the spread of Covid-19 that can be suppressed, loosening policies that increase mobility so that public consumption can increase and investment conditions continue to improve. In terms of fixed interest rates, with policies such as those that have been implemented by Bank Indonesia through expansion in loosening liquidity to encourage the availability of liquidity in the banking sector, credit and sales of automobiles are projected to increase.

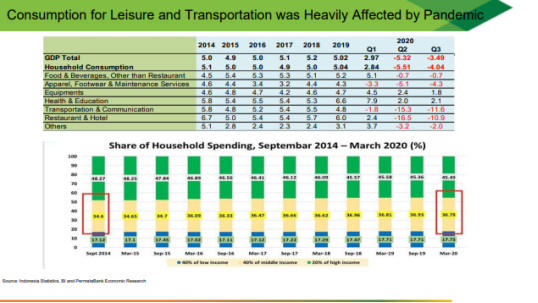

Thelargest contribution to national consumption comes from 40% of the lower class and 20% of the upper class. Because the middle and upper class people cannot spend, an initiative from the government is needed in the form of a stimulus package. This is used in an effort to revive the consumption of the middle and upper class, one of which is by providing confidence through handling Covid-19 which is quite good. The demand side shows a condition of slowing consumption and investment due to low demand. From the supply side, there are four biggest contribution sectors, namely manufacturing, agriculture, trade and construction, it turns out that there is only one sector that is still growing positively, namely the sector agriculture. Therefore, this will require that Indonesia’s digital development must be accelerated, especially for MSME. Digitalization was carried out as a response to policies to balance structural reforms and economic recovery.

If you look at the future economic prospects based on the data above, only China can touch the level GDP baseline or full recovery. This means that the Indonesian state will not experience a full recovery. It is estimated that the Indonesian economy will return to the 2019 GDP level in approximately two years. To illustrate the crisis that occurred in 1997-1998, it can be seen that at that time there was a crisis that was more severe than the current crisis and it took 5-6 years to return GDP to pre-crisis levels. This is intended so as not to be pessimistic because this crisis is not the end of the world.

Covid-19 caused uncertainty quite high. This is worrying because in contrast to the observations observed by observers at the beginning of the crisis, Covid-19 based on its hypothesis and theory was initially considered light because the economic crisis caused by natural disasters including a pandemic was only temporary. This crisis caused various weaknesses in the economies of various countries. Uncertainty makes people tend to delay, especially in spending and causes a scare effect.

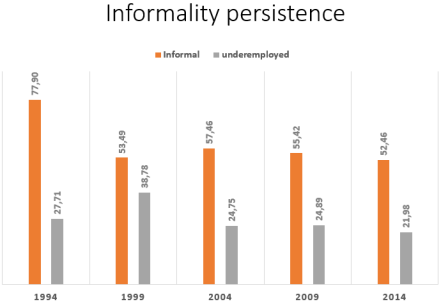

There are two categories of community groups, namely the middle class people who tend to follow what the government orders and those who do not follow what the government orders. These two categories of community groups are vulnerable to having an impact on the economy. The impact that occurred during the pandemic was an increase in unemployment, many people lost their formal jobs, which resulted in an increase in the severity of unemployment due to the Covid-19 crisis.

The Covid-19 pandemic resulted in a tendency for workers to then work in the informal sector, the number of workers working in the informal sector is something that is contrary to the modern economy, where the informal sector should be reduced and after a while must be eliminated. The thing of concern in the Covid-19 crisis is modernizing the labor market.

The sectors that experienced the biggest decline during the crisis were the manufacturing and construction sectors, where during the current crisis most of these workers moved to agriculture, forestry and fishing and wholesale and retail trade, repair of motor vehicles and motorcycles, both of which are low productivity sectors. What is adding to the concern is that it is not common in other countries. This means that this is something that needs to be assessed for whether it will be good or bad.

Increase in the situation in which Covid-19 is accelerating digitization. This is related to stagnation in the formalization of jobs accompanied by stagnation of the number of workers entering manufacturing so that many workers who leave agriculture do not return to the industry but instead return to informal services, there is a hypothesis that inequality in Indonesia occurs. The past one to two decades has seen a fairly similar rate of increase to inequality in income generated from employment. The theory regarding this is routine technical change bias or techincal change skill bias which is the loss of jobs because they are replaced by computers and algorithms which then result in job polarization.

Based on the data above, it can be seen that the type of work that is abstract in nature has increased, while work that is routine manual has decreased, this indicates that the occurrence of RBTC (routine bias technical change) in Indonesia. The connection with Covid-19 is to accelerate this process so that people who leave jobs, especially manufacturing, are not welcomed back when they recover for this reason.

There are two very large digital economic opportunities in Indonesia, namely the financing gap where there are still many Indonesians who do not have access to banking products and of the 60 million MSMEs there are still 70% who also do not have access to banking. Fintech Indonesia with its potential and development is expected to be one of the steps for Indonesia’s digital transformation going forward.

When the trend of banking credit growth is relatively down, P2P lending growth has increased, this has become an alternative financing for MSMEs that do not yet have adequate access to banking business credit so that they can take advantage of fintech. The increase resulted in digital transactions which also increased during the pandemic.

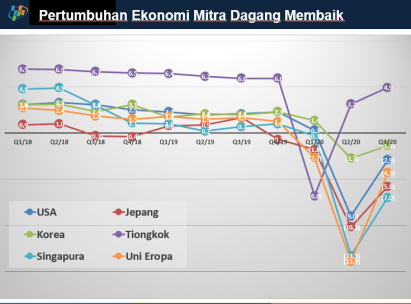

Potential national economic growth that will improve can be seen from the economic growth of West Java’s trading partners which is starting to improve. This is a potential for the national export market which will result in demand growth and will encourage the supply side which will begin increase production, so that economic growth will begin to improve. The prediction of Indonesia’s economic growth in 2021 based on world institutions starting from the IMF is 6.1%, the World Bank is 4.8%, the ADB is 5.3% and the OCD is 5.2%, meaning that there is confidence that Indonesia’s economic growth will improve where Q4 will be parameter whether it is true that the economy has started to improve. West Java has a very large economic role and second place in the contribution to national GDP, so that if the West Java economy improves, the national economy will also improve.

One of the efforts made by the local government is to develop the “REBANA” area in which there is a Rebana triangle including the development of the Patimban Port in the Subang area with a total investment estimated at Rp. 44 trillion, this is an opportunity that in 2021 there will be a large enough investment. This investment effect will cause a multiplier effect on the sectors that support this development, so that there will be a potential that the economy will begin to improve in 2021.

Based on a survey conducted conducted by BPS related to the impact of Covid-19 on business actors, there were 86.12% of companies that experienced a decrease in revenue, 11.40% of companies experienced no change in revenue, and 2.48% of companies experienced an increase in revenue. This means that the Covid-19 pandemic affects many companies except those related to companies in the health sector. Based on a survey conducted with Bukalapak, there was an increase intrade online by 5000%.

In general, 8 out of every 10 UMK and UMB companies tend to experience a decrease in demand because customers are affected by Covid-19. Then, 7 out of every 10 companies face obstacles due to their business partners being very badly affected or unable to operate normally both on the MSE and UMB scale. Then around 56.41% MSEs and 72.47% MSEs face financial constraints related to employees and operations. One of the strategies that can be used for economic recovery is to increase demand. Many companies have problems related to how long they can survive with the current conditions, where there are 17.40% of business actors who claim to be able to survive in their current conditions for a maximum of three months since July 2020, if there is no change in operations and assistance, then 22.22% of the business actors believes it will be able to survive its current condition for more than three months, even without any changes in operations and assistance. This means that the policy focus must make how these companies can come back to life, for that the second strategy that can be done is to provide assistance to business actors both to MSEs and MSEs, and the third strategy that can be done is to focus on sectors with BL and high FL.

The Covid-19 pandemic situation has resulted in stagnation of various economic machines ranging from consumption and investment. The role of the government is important in dealing with this, so that the State Budget is one of the most important Instruments. Fiscal policy moves quickly to respond to the pandemic and makes adjustments to protect the economy, by:

1. Publishing PERPPU No.1/2020

2. National Economic Recovery Program

3. State Budget Adjustments

4. Burden sharing with Bank Indonesia

The following is a comprehensive policy program to save lives and the economy:

In 2021 it is projected that there will be economic recovery, so that the trend of economic recovery is expected to continue to improve going forward. For this reason, it is very important for every individual and community group to maintain discipline in health protocols so economic recovery can continue. The government also needs to prioritize handling Covid-19, therefore health issues need to be improved and accompanied by starting to move economic sectors that are not significantly affected, maintaining domestic market growth, maintaining public purchasing power, focusing on the continuity of MSME businesses, stimulus policies relieve business actors and workers, increase fiscal stimulus, formulate procedures for vaccine distribution, control the realization of budget absorption and encourage the expansion of the digital economy in Indonesia. Economic growth in 2021 is expected to return to the 5% level, the economic contraction due to Covid-19 is not as bad as during the Asia financial crisis, so it is expected to be a supporting capacity for better and faster economic recovery.