By : Research Division HIMA ESP FEB UNPAD

- Global Economic Uncertainties and Challenges

This year has a gloomy economic projection. Major economies around the world are predicted to have slower growth. The US economy is predicted to grow by 2.3% this year, below the 2.9% in last year and only 1.8% next year. China’s economy is also predicted to slow down from 6.6% in last year to 6.2% this year. This slowdown is being caused by many factors which are rising protectionism and populism, high global debt ratio, geopolitical risks, slow trade growth, and the slowdown of commodity prices. The most notorious of these is the US-China trade war. We are still waiting for the result of Phase One of the US-China trade deal. If the negotiations are going into a deadlock, we can expect the trade war to intensify next year.

Figure 1 Source: Taufik Saleh, Bank Indonesia

This global economic uncertainty has pushed central banks to start expansionary monetary policies. Central banks around the world are decreasing their interest rates to increase money supplied in the economy and stimulate the business cycle. In the first and second quarters of 2019, Bank Indonesia anticipated the US Federal Reserve to raise its interest rate. Turns out the Fed decreased their interest rate instead due to low inflation which helps maintain rupiah’s value. Central banks have other tools other than interest rates, such as increasing market liquidity. For example, Europe has initiated an asset purchasing program which involves the purchase of private bonds and China is lowering their medium lending facility. All these policies will have an impact on Indonesia’s current account balance.

The trade war also has impacted China. The Chinese economy is predicted to grow by only 6% next year, which will be the lowest since 1992. When the trade war was announced, China is looking for new trade partners. Due to the rising labour wage in China, Chinese companies are looking to move their production facilities to ASEAN countries, such as Vietnam where the wages are lower, so they can produce their products there and export it from Vietnam, effectively circumventing US tariffs. This includes Indonesia, where several steel mills projects are being planned to be built in several islands through Chinese investments.

Looking at the financial crisis in 2008, Indonesia was not severely affected by the crisis. This is due to the Indonesian economy not fully integrated into the global economy, as Indonesia still has a low trade to GDP ratio of 43% which is much lower compared to its neighbours. The issue with our current situation is that Indonesia has high trade dependencies on China. China is Indonesia’s largest trade partner by far, consisting of 19.7% of Indonesia’s trade value. This is much higher compared to Indonesia’s trade with the US which is only 7.8% of Indonesia’s trade value, which Indonesia also has a trade surplus. Our largest exports are mineral fuels (coal and oil) and animal and vegetable oil, mostly CPO. China is Indonesia’s largest coal buyer. It is feared that if China’s growth slowing down, the demand for Indonesia’s coal and CPO will also go down.

Indonesia’s Total Trade Value with ts Trade Partners 2018

Figure 2 Source: Andry Satrio Nugroho, INDEF

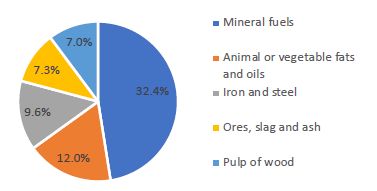

Indonesia’s Top 5 Exports to China

Figure 3 Source: Andry Satrio Nugroho, INDEF

Indonesia’s economy is reliant on CPO. Meanwhile, Indonesia is facing difficulty in entering other markets. The EU is threatening to ban palm oil imports, Indonesia is losing to Malaysia in the Indian market, and biodiesel has not been able to enter US market. As long as there is no diversification, Indonesia will always depend on the domestic market and commodity price. Meanwhile, Thailand has high added value exports and Vietnam’s export is dominated by electronic products. Indonesia has vast natural resources, but its industrial structure needs reform.

Indonesia’s Export Profile

Figure 4 Source: Wikimedia Commons

- Domestic Economic Performance

Despite the global economic conditions, Indonesia has been able to maintain a stable economic growth of around 5%. However, this trend is not new. Indonesia has been the most stable economy in the region since 2002, it has low volatility compared to neighbouring countries. Indonesia has the lowest standard deviation of annual GDP growth rate, followed by Australia. This stability in recent years is caused by smaller trade exposure, relative political stability, and generally good record in macroeconomic management and crisis risk mitigation.

Figure 5 Source: Martin Siyaranamual, UNPAD

Indonesia’s current economic growth is manageable throughout the archipelago. Sumatera’s economic growth tends to be under the national average, with provinces of North Sumatera, West Sumatera, and Lampung leading. Kalimantan still mostly relies on primary commodities like coal and oil, with the highest contributors are Central Kalimantan, East Kalimantan, and North Kalimantan. Sulawesi excels in primary commodities such as agriculture and minerals, although its growth is relatively low. Papua and the Moluccas have the lowest economic growth below the national average, while Bali and Nusa Tenggara are still above the national average. Meanwhile, economic growth is highly variative in Java. The highest one goes to Jakarta. Jogjakarta and Central Java also perform well due to the new airport project and the new industrial area in Kendal respectively. West Java and East Java do not perform as well due to the manufacturing slowdown.

Figure 6 Source: Taufik Saleh, Bank Indonesia

Another major factor in Indonesia’s economic stability is the large portion of domestic household consumption in the national economy. Most of the large consumption is driven by low-income households, which is also pushed by government transfers. In order to maintain a high level of consumption, the government has to maintain purchasing power while concerning its fiscal capabilities. Indonesia still has a healthy domestic household consumption growth at 5.01% in Q3 2019, although it is lower than the previous quarter at 5.17%.

Investment tends to slow down. Investment in Q3 2019 grew by 4.21% which is lower than the previous quarter at 5.01%. Building investment tends to grow, stimulated by government strategic infrastructure projects, while non-building investment, such as machinery investment, tends to go down. Gross fixed capital contribution to GDP is still satisfactory. Investment growth on vehicles still low at 4.2%, machine investment tends to go down. This slow investment environment can be attributed to the regulations in the provincial regions and below. While our FDI performance is adequate, its leverage on GDP is low due to our investment efficiency. If Indonesia can lower its Incremental Capital Output Ratio, Indonesia can have an even higher economic growth.

Figure 7 Source: Taufik Saleh, Bank Indonesia

Regulations and institutions become the main obstacle for FDI. There are several reasons which are:

- Labour regulations, especially regarding hiring environment. For example, severance pay in Indonesia is very high which makes companies to outsource a large portion of their labour. When people become permanent workers, it is very expensive for companies to fire them. Too many outsourcings also mean that there will be a lack of trainings. And then we have the complex minimum wage laws, with every region have their own regulations. When a company tries to move its production to another region, it will have to face another different set of laws.

- Human resource situation. Indonesia still has fewer high-skilled labour, which becomes a middle and long term constrain. Educational quality wise, we still far behind in PISA scores. Regarding health, maternal mortality is still high and sanitation quality is also lacking. Indonesia is ranked third in the world for number of people practicing public defecation.

- Fiscal condition. We still have fiscal problems as our tax ratio is still lower than 12% and non-tax revenue from oil and gas continue to face structural decline. There is a structural problem in Indonesia’s ability to collect taxes as overall revenue collection grows more slowly than inflation. Indonesia’s limited fiscal resources constrains Indonesia’s ability to pursue its development agendas. A major tax reform is needed to correct the current tax ratio.

- Indonesia’s institutional quality is still low. Corruption is still rampant, and the bureaucracy is inefficient. There is also a lack of coordination between government bodies and policies with similar agendas.

- Lastly, we still require more infrastructure to increase our connectivity as Indonesia has large geographical constrains.

The investment-based labour absorption is also still low, investment could not absorb the labour force in certain sectors. It seems that investment is focused on the capital-intensive sectors rather than the labour-intensive ones. From 2008 to 2011 the majority of FDI goes to the tertiary or the service sector, only the rest goes to the secondary or the manufacturing sector. This is a concern for Indonesia as a country with abundant low-skilled labour force, as the sectors with large low-skilled labour absorption are manufacturing and agriculture, compared to the service sector which is more high-skilled oriented. From 2012 to several years ahead the majority of FDI went to the secondary sector, but in 2019 the trend goes back to the service sector.

Indonesia is in danger of experiencing premature deindustrialization as its manufacturing sector contribution is decreasing throughout the years since the early 2000s (inverted u-shape). Deindustrialization is a common phenomenon in developed countries where it is associated with loss of jobs, deepening inequality, and a downturn in innovation. However, Indonesia is a developing country which makes this deindustrialization premature. Indonesia’s manufacturing sector could die out before it has a chance to bloom. Deindustrialization can have a major political impact, as workers go unemployed due to factories closing and politicians pursuing populist policies. While deindustrialization is happening around the world, Indonesia’s deindustrialization rate is 8% in the past ten years, one of the fastest in the world.

Manufacturing Sector Contribution to GDP

Figure 8 Source: Andry Satrio Nugroho, INDEF

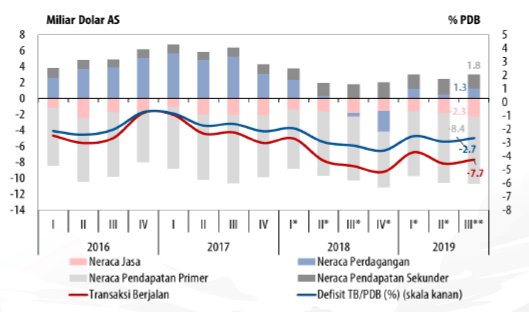

Indonesia’s balance of payment deficit is improving from 2 billion USD in Q2 2019 to 46 million USD in Q3. This improvement is supported by the improving Current Account Deficit (CAD) and relatively high financial and capital transaction surplus. CAD is improving Q3 2019 supported by the improving oil and gas trade balance and the decrease of primary income balance due to the low dividend repatriation and foreign debt payment. However, one of our speakers, Mr. Siyaranamual argued that excessive concern over the CAD is unnecessary and that the government should allow rupiah’s value to be more volatile as to let the market mechanism correct the CAD through the exchange rate and exports. The concerns surrounding the CAD is that foreign investors will pull out of Indonesia, but according to economic theory, this will cause our rupiah to depreciate, increase our exports, and improve our CAD. The Marshall-Lerner Condition is correct if the inflation rate is low, and we do have a low inflation rate. All that is left is the government’s willingness.

Current Account Balance

Figure 9 Source: Taufik Saleh, Bank Indonesia

Foreign currency reserve stays strong at 126.7 billion USD, capable of financing 7.4 months of imports and 7.1 months of imports and government foreign debt payment. Rupiah’s value is still improving, appreciating by 0.42% on average in November, supported by foreign currency inflow from exports and foreign capital investments.

Foreign Reserves (billions of US$)

Figure 10 Source: Eka Chandra Buana, BAPPENAS

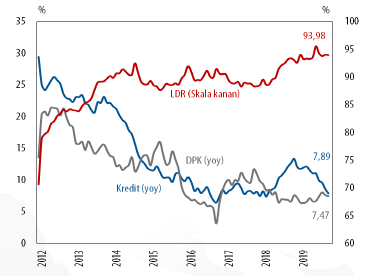

Credit growth tends to slow down across Indonesia from 8.59% in August 2019 to 7.89% in September 2019. Credits can support manufacturing performance. Indonesia still has a problem regarding the low credit provided by the financial sector to the private sectors. However, this year, credit growth remains slow as most companies reluctant to expand their business due to the high level of uncertainty. At the same time, people do not prefer to save their money due to the low-interest rate compared with other investment instruments such as government bonds. As a result, there is a lack of liquidity in the financial sector.

Figure 11 Source: Taufik Saleh, Bank Indonesia

- Economic Projections

Various institutions predicted different levels of projections. Bank Indonesia projected Indonesia’s overall economic growth for 2019 to be around 5.1%. Meanwhile, low inflation is predicted to continue with 2019 CPI inflation around 3.1%. CAD is predicted to lower to 2.7% of GDP. Both credit and Third-Party Fund is predicted to grow by 8% in 2019.

Figure 12 Source: Taufik Saleh, Bank Indonesia

Indonesia’s economy is predicted to grow by 5.2% in 2019 and 5.3% in 2020 by the World Bank, 5.1% in 2019 and 5.2% in 2020 by the Asian Development Bank (ADB), and 4.8% in 2019 and 4.9% in 2020 by the International Monetary Funds (IMF).

Institute for Development of Economics and Finance (INDEF) also have its own projections on Indonesia’s economy in 2020. They predicted the economy to grow by 4.8%, far from government’s target of 5.3%. Exchange rate prediction relatively the same with the government’s between Rp14.400 – Rp14.500 per USD. However, it is not known whether the Fed will raise the interest rate. Inflation stays at 3.5% and unemployment rate at 5.1%.

Figure 13 Source: Andry Satrio Nugroho, INDEF

- Government Policies and Targets

Government institutions like Bank Indonesia (BI), Ministry of Finance, and Ministry of National Development Planning (Bappenas) all conduct macroeconomic studies, the difference being that BI focuses on monetary policies, Ministry of Finance on fiscal policies, and Bappenas on lowering open unemployment rate, increasing HDI, and lowering the Gini ratio. High economic growth will not be that meaningful if unemployment is high, inequality is high.

Bank Indonesia policies for next year are to keep the 7-day Reverse Repo Rate at 5%, the Deposit Facility Rate at 4.25%, and the Lending Rate at 5.75%. BI’s policy will focus on accommodative monetary policy and a consistent one with the projected inflation rate around the target, maintaining external stability, and efforts to keep the economic growth momentum in the middle of the global economic downturn. Other BI policy instrument mixture will also be directed to support economic growth. Macroprudential policies stay accommodative to stimulate bank credit flow and expanding funding for the economy while maintaining the financial system stability.

Bappenas’ 2020 macro policy directions are increasing Indonesia’s potential growth, maintaining macroeconomic stability, and ensuring inclusivity and economic development sustainability. From 2020-2024, with the newly elected president Joko Widodo, Bappenas has a responsibility in turning the visions and missions of the new president into a concrete policy. Their long-term targets are that Indonesia will avoid the middle-income trap by 2036, becoming one of the 5 largest economies in the world and making Eastern Indonesia’s contribution to 25% of the national economy by 2045.

For the next 5 years, Bappenas targeted 6% economic growth on average and poverty rate at 7%. Bappenas is aiming high on the economic growth so that other goals may be achievable. In a meeting with the president, Bappenas provided the president with 3 scenarios of mid-term economic growth: high scenario, moderate scenario, and low scenario, assuming the exchange rate and inflation rate are maintained. The president chose the first scenario. Indonesia requires high economic growth in the 2020-2024 period in order to become a high-income economy by 2036. To achieve these targets, Bappenas identified several focuses:

- Pushing investment in the manufacturing sector which has high value-added and transfer of technology, simplification of investment procedure, and investment in industrial areas and Special Economic Regions (KEK).

- Turning fiscal condition to become a stimulus for Indonesia’s economic growth with loosened fiscal policy and fiscal policies that supported investment in manufacturing sector.

- Maintaining net exports by improving the tourism industry as a safeguard for Indonesia’s CAD and import management through import substitution and safeguards.

- Increasing productivity and pushing innovation and technology transfer to achieve industrialization in order to create more jobs and more resilient domestic economy.

For all these to be achieved, there must be a common development direction so that all policy implementations are consistently coordinated and supervised. All coordinator ministers have to be on a single standing to compose mid-term development programs according to the president’s visions and missions. To achieve the 6% targeted economic growth, there needs to be strong cooperation between the central government, the regional governments, and the public.

President Widodo also has several new large far-reaching programs that raise some concerns. One of the biggest projects, the capital relocation from Jakarta to East Kalimantan with the relocation predicted to start by 2024. We have to see this project from a cost and benefit analysis perspective. Indonesia is not the first country to move its capital, but it is the first to move it across the sea.

Cost-wise, the government has reported an investment requirement for the public and private sector of Rp466 trillion or US$33 billion according to the former National Development Planning Minister, Bambang Brodjonegoro. However, this number may be a large underestimate of the overall requirement since a new capital will need good infrastructure. Secondly, the costs of this project are ongoing, not just up front. Third, this project will displace the scarce resources from other priorities. Fourth, there will be costs beyond the market prices, which are environmental and social implications/costs. Lastly, regardless of the relocation, Jakarta will still need to be saved. There are 7 million civil servants in Jakarta. Moving the capital will only move 7 million people out of a daily population of around 40 million. In any case, Jakarta will still need fixing. Additionally, there also megacities who work well as a capital such as Tokyo, Paris, and London.

Another major program is the Pre-Employment Cards (Kartu Pra-Kerja). Indonesia still has challenges providing decent jobs in large quantities and, as explained before, still lacking high-skilled workers. The president has announced pre-employment cards starting from 2020. The aim is to fund vocational training opportunities for the unemployed to help them back into the workforce. The program targets 2 million unemployed people and an initial budget of Rp10.3 trillion or US$726 million. There is also a concern that this program will create a moral hazard, especially if the formal and informal sectors of employment are equally large. It is suggested that the government focuses on reforming the labour regulations first.